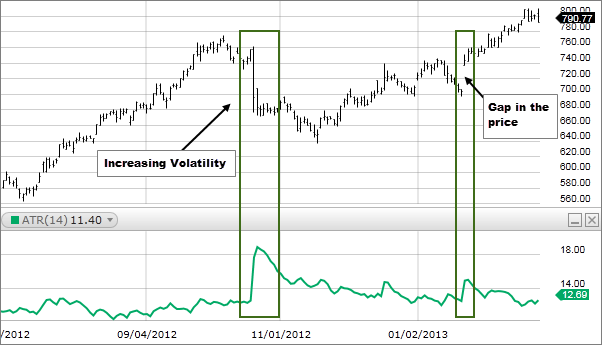

Average True Range Percentage

:max_bytes(150000):strip_icc()/ATR-5c535f8fc9e77c000102b6b1.png)

Average True Range Atr Definition

What Is Average True Range Fidelity

Average True Range Atr Chartschool

How To Use Average True Range True Trading Strategies Average

Moving Average Strategies For Forex Trading

True Strength Index Tsi Technical Indicators Indicators And Signals Tradingview

Description average true range percent atrp expresses the average true range atr indicator as a percentage of a bar s closing price.

Average true range percentage.

How To Download Install Atr Indicator For Mt4 And Mt5

Scalping Forex Scalpingforex Forex Forex Trading System Binary

Choppiness Index Indicator Trading Strategy Stockmaniacs Trading Strategies Cryptocurrency Trading Trend Trading

Make 98 Profit Only In 30 Seconds Too Good To Be True With This Website You Can Trade And Make Easy Mercado De Acoes Investimento Investimento Financeiro

Monitoring Of Multiple Markets Timetotrade Community How To Get Rich Intraday Trading Online Trading

9qhdpc 41lowrm

Square The Range Trading System By Michael S Jenkins Sacred Traders Jenkins Trading System

Tiw8i54tv3y69m

S6k2u2mvvws6am

9tppj04maqj3km

S Viuxhhpoytgm

Doublecci Woodies Metatrader 4 Forex Indicator Forex Woodies Chart

My2 Nkyxrgutlm

5cpcp0pnkmxavm

Wbgqjz39xd6jxm

8i6qi7zjgmpfjm

Tjw0h Pg8afdm

An Introduction To True High True Low Average True Range Atr Is Known As A Volatility Indicator Which Was Blog Marketing Forex Trading Tips Stock Market

Https Encrypted Tbn0 Gstatic Com Images Q Tbn 3aand9gct6scdz3kdcinsn4yvc Samjfeq0bvpwp5ukrg38ppkt3unmy9q Usqp Cau

Npt1ruolpjw2lm

B Uy S3pqbrr6m

Vjhkl2ccgntr5m

Make 98 Profit Only In 30 Seconds Too Good To Be True With This Website You Can Trade And Make Easy An Trading Charts Stock Options Trading Forex Trading

Pin On 044 Investing Fintech

Source : pinterest.com